Owning a landed house in Singapore is a significant milestone that many aspire to achieve. Known for their spaciousness, privacy, and potential for long-term appreciation, landed houses represent the pinnacle of property ownership in Singapore. However, the financial commitment required to purchase such a property is substantial, and understanding the financial requirements is essential for potential homeowners.

In this article, we will explore the key factors that determine how much you need to earn to buy a landed house in Singapore. We’ll delve into the costs associated with purchasing and maintaining a landed property, the financial metrics banks use to assess your loan eligibility, and how you can plan your finances to make this dream a reality.

Understanding the Cost of a Landed House in Singapore

The first step in determining how much you need to earn to buy a landed house in Singapore is understanding the costs involved. The price of a landed house varies widely depending on factors such as location, size, type of landed property (e.g., terrace house, semi-detached house, bungalow), and the overall condition of the property.

Location

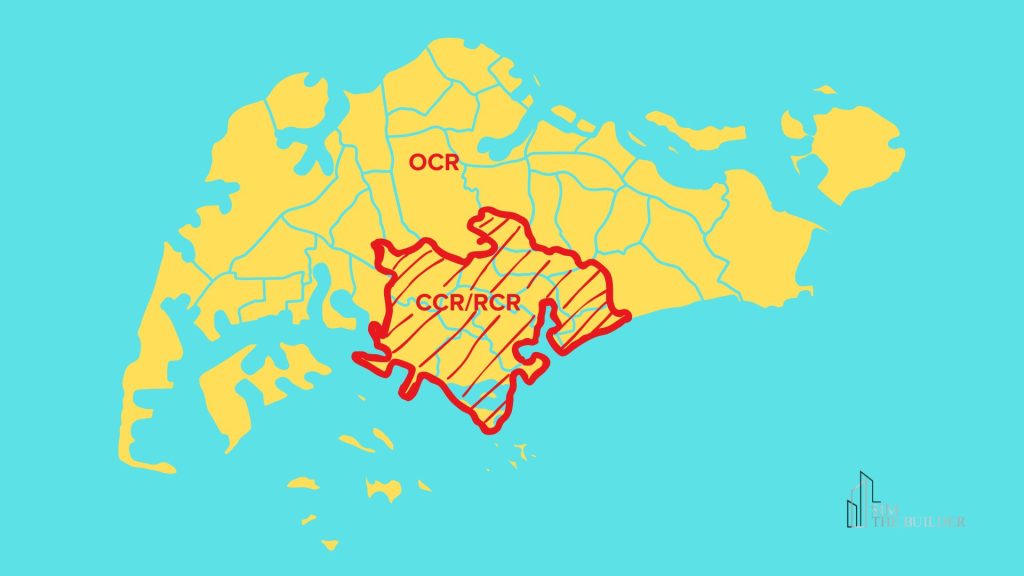

Core Central Region and Rest of Central Region (CCR & RCR): Landed houses in prime districts like District 9 (Orchard, River Valley), District 10 (Bukit Timah, Holland Road), and District 11 (Newton, Novena) are the most expensive. Prices here can easily exceed S$10 million for a good-sized property.

Outside Central Region (OCR): Landed houses in suburban areas like District 19 (Serangoon, Hougang) or District 28 (Seletar) are more affordable but still come with a hefty price tag, often ranging from S$2 million to S$5 million

Type of Landed Property

Terrace Houses: These are typically the most affordable type of landed property, with prices starting from around S$2 million in the OCR and going up to S$10 million or more in the CCR

Semi-Detached Houses: These offer more space and privacy than terrace houses, with prices ranging from S$3 million to S$15 million.

Bungalows: The epitome of luxury, bungalows are the most expensive type of landed property, with prices starting from S$5 million and going up to S$100 million or more for a Good Class Bungalow (GCB) in the CCR.

Read more: Types of Landed House in Singapore

Property Size

The size of the property, both in terms of land area and built-up area, plays a crucial role in determining the price. Larger plots of land naturally command higher prices, especially in land-scarce Singapore.

Condition of the Property

A well-maintained or newly renovated house will cost more than one that requires significant repairs or renovation. However, buying a landed house in need of refurbishment can be an opportunity to design your dream home, especially if you’re planning to engage a design and build construction company.

Down Payment and Mortgage Requirements

Once you have a rough idea of the property price range you’re interested in, the next step is to consider the down payment and mortgage requirements. In Singapore, the maximum loan-to-value (LTV) ratio is 75% for your first property loan, meaning you’ll need to pay at least 25% of the property price upfront as a down payment.

Down Payment

The down payment is divided into two parts: a minimum of 5% must be paid in cash, and the remaining 20% can be paid using your CPF Ordinary Account (OA) savings or cash.

For example, if you’re purchasing a S$5 million property, the minimum down payment would be S$1.25 million, of which at least S$250,000 must be paid in cash.

Mortgage Loan

The remaining 75% of the property price can be financed through a mortgage loan, subject to the Total Debt Servicing Ratio (TDSR) framework, which limits the amount of your gross monthly income that can be used for debt repayments, including the mortgage.

Total Debt Servicing Ratio (TDSR) and Your Income

The TDSR framework by the Monetary Authority of Singapore (MAS) is a key factor in determining how much you need to earn to afford a landed house in Singapore. Under this framework, your total monthly debt obligations cannot exceed 55% of your gross monthly income. This includes not just your mortgage payments, but also any other loans you may have, such as car loans or personal loans.

Calculating Your TDSR

To calculate your TDSR, you first need to estimate your monthly mortgage payment. This depends on the loan amount, interest rate, and loan tenure.

For example, if you’re taking a S$3.75 million loan (75% of a S$5 million property) at an interest rate of 2% per annum over a 30-year tenure, your monthly mortgage payment would be approximately S$13,874.

Minimum Income Required

To meet the TDSR requirement, your gross monthly income should be sufficient to cover your mortgage payment and any other debt obligations while staying within the 55% cap.

If your only debt obligation is the mortgage payment, you would need to earn at least S$25,225 per month to qualify for the loan. This translates to an annual income of approximately S$302,700.

You can improve your TDSR by either increasing your income or reducing your debt.

A useful tool to quickly calculate your TDSR is to go to Property Guru TDSR Calculator.

Additional Costs and Considerations

Beyond the purchase price and mortgage, there are several additional costs associated with buying a landed house in Singapore. These include stamp duties, maintenance costs, property taxes, and renovation expenses.

Stamp Duties

Buyer’s Stamp Duty (BSD): This is calculated as a percentage of the property price, with rates ranging from 1% to 4% depending on the property’s value.

Additional Buyer’s Stamp Duty (ABSD): If you’re purchasing a second or subsequent property, you’ll also need to pay ABSD, which can range from 12% to 30% depending on your residency status and the number of properties you own.

A useful tool to quickly calculate your BSD or ABSD is to go to Property Guru Stamp Duty Calculator.

Maintenance Costs

Landed properties generally require more maintenance than condominiums or HDB flats. This includes costs for landscaping, pest control, roof repairs, and general upkeep.

These costs can add up to several thousand dollars per year, depending on the size and condition of the property.

Property Taxes

Property taxes for landed houses are higher than for other types of residential properties. The tax rate is progressive, with higher rates for non-owner-occupied properties.

Renovation Costs

If you’re purchasing an older property or one that needs refurbishment, you’ll need to budget for renovation costs. These can range from S$100,000 to S$1 million or more, depending on the extent of the work and the quality of materials used.

How much to earn per month?

Assuming you want to buy a S$5 million landed property and you have no other debt obligations. Here is the breakdown:

Down Payment

- 25% of the property price is required as a down payment.

- For a S$5 million property, this would be S$1.25 million.

- At least 5% of this (S$250,000) must be paid in cash, with the rest potentially covered by CPF OA savings or additional cash.

Mortgage Loan

- You can finance up to 75% of the property price through a mortgage, which would be S$3.75 million.

- Assuming an average of 3% interest rate over a 30-year loan tenure. The monthly mortgage repayment would be approximately, S$15,810.

Total Debt Servicing Ratio (TDSR)

- To meet the Total Debt Servicing Ratio (TDSR) requirement, where your monthly debt obligations cannot exceed 55% of your gross monthly income, you would need to earn at least:

- S$15,810 ÷ 0.55 ≈ S$28,745 per month.

- This translates to an annual income of approximately S$344,940.

This amount stated is the bare minimum. You must take into account your other financial obligations.

Buying a landed house in Singapore is a significant financial commitment, but with careful planning and the right support, it is achievable. By understanding the costs involved, planning your finances, and engaging professionals to help with the design and construction process, you can make your dream of owning a landed house a reality.

If you’re planning to purchase a landed house that requires renovation or you’re considering building your dream home from scratch, engaging a design and build renovation company can be a wise decision. The primary goal of design and build renovation is to eliminate the middleman and simplify the entire construction project pipeline, thus saving time and money for the client.

Engage us today.

At Sim The Builder, we specialise in designing and building beautiful, functional landed homes tailored to our clients’ needs. Whether you’re looking to renovate an existing property or build a new home from the ground up, our team of experienced professionals is here to guide you every step of the way.

Our design and build services include everything from initial consultations and architectural design to construction management and final handover. We work closely with our clients to ensure that every detail is perfect, and we pride ourselves on delivering projects that exceed expectations.

If you’re considering purchasing a landed house in Singapore and want to learn more about how our services can help you achieve your dream home, contact us today for a consultation. Let us help you turn your vision into reality.