Introduction

Purchasing a landed property is more than just acquiring a home; it’s about investing in a lifestyle and securing long-term stability and growth. Unlike condominiums or HDB flats, landed homes offer the luxury of privacy, spaciousness, and the freedom to shape your living environment. Yet, the journey of owning one involves navigating a maze of legal requirements, securing financing, and considering house construction or renovation possibilities.

Whether you’re a first-time buyer, an experienced investor, or looking to upgrade to a larger space, a well-crafted roadmap is essential. This guide covers everything you need to know about buying landed property in Singapore. We’ll delve into the key differences between freehold and leasehold properties, explore zoning regulations, and highlight financing options and house construction considerations. With this knowledge in hand, you’ll be empowered to make choices that reflect both your immediate needs and long-term goals.

Key Takeaways

- Understanding the different property types and ownership options is crucial in making an informed investment decision in Singapore’s real estate market.

- Performing thorough legal checks, such as title searches and caveat checks, ensures that the property you’re considering is free from disputes or encumbrances.

- Securing the right financing is essential, whether through personal savings, loans, or CPF funds, and it’s important to understand the various financial requirements involved.

- From initial research to designing your ideal home, proper planning and expert assistance can make the property buying and building process smoother.

Understanding Landed Property in Singapore

The landed property market presents a variety of options, where the type of ownership significantly impacts both long-term value and investment potential. The two main types, freehold and leasehold, offer their own advantages and considerations. By exploring these differences, you can make a more informed decision that aligns with your financial goals and lifestyle needs when buying landed property in Singapore.

Freehold vs Leasehold: What’s the Difference?

A. Freehold Property

Owning a freehold property means you have indefinite ownership of both the land and the building. This permanence offers stability and flexibility, making freehold properties highly desirable. As a long-term investment, they often hold or increase in value and can be passed down through generations. However, their desirability comes with a higher price tag, reflecting the lasting security they provide.

B. Leasehold Property

On the other hand, leasehold properties come with a fixed ownership period, typically 99 years. Once the lease expires, ownership reverts to the government unless an extension or redevelopment is pursued. As the lease shortens, the property’s value may decrease, affecting its resale potential. However, leasehold properties are generally more affordable upfront, making them an appealing option for buyers with a set budget.

Which One Should You Choose?

- Freehold: Ideal for those seeking long-term security, freehold properties retain their value across generations. It’s an excellent choice for those investing for the future or desiring stability in their home.

- Leasehold: A practical choice for those looking for affordability or planning to stay for a set period. Just keep in mind the potential for reduced resale value as the lease runs down.

Your choice should align with your financial goals and plans for the future. If stability and long-term growth are important, freehold may be the better option. If budget and flexibility are your priorities, leasehold could offer the best entry into the landed property market..

Different Types of Landed Property in Singapore

Landed properties come in various forms, each offering distinct features, space, and price points. Whether you’re after privacy, more room to grow, or a budget-friendly option, understanding these types can help you find the right fit for your needs. Here’s an overview of the most common property types to help guide you as you navigate the process of buying landed property in Singapore.

- Terrace House: A row of connected homes offering a practical balance of space and affordability. These are often found in well-established neighbourhoods, making them ideal for those seeking community living with easy access to amenities.

- Semi-Detached House: A home that shares one wall with a neighbour, providing more privacy and outdoor space than a terrace house. It’s perfect for families looking for extra room but at a more affordable price than a fully detached property.

- Conservation House: Located in heritage areas like Tiong Bahru, these charming homes have a unique historical appeal. However, due to their preservation status and cultural value, their distinctiveness comes with a higher price tag.

- Bungalow: A standalone house offering generous outdoor space and a sense of privacy. Typically situated in suburban areas, bungalows offer a luxurious living experience with room to breathe.

- Good Class Bungalow (GCB): Prestigious, expansive homes found in Singapore’s most sought-after locations. Known for their exclusivity and luxury, GCBs are often seen as symbols of wealth, with strict ownership regulations in place.

- Cluster House: These modern homes are part of a well-planned development, offering shared amenities like pools and gyms. They combine the benefits of space with the convenience of communal facilities, typically being more affordable than standalone bungalows.

Why Title Searches Are Essential When Buying Landed Property in Singapore

1. What is a Title Search?

A title search is an essential step in property buying, especially when buying landed property in Singapore. It involves checking the legal ownership of the property and uncovering any potential claims, debts, or encumbrances tied to it. By conducting a title search, you ensure that the property has a clear and unchallenged title, giving you peace of mind as you move forward with your purchase.

2. Why It’s Important

A title search is a critical step when buying landed property in Singapore. It ensures that the property is free from any disputes, unpaid debts, or legal claims. This check confirms that the seller is the rightful owner and has the authority to sell the property. By conducting a title search, you protect yourself from inheriting any unresolved financial issues, such as unpaid taxes or ongoing ownership conflicts. This step provides peace of mind, allowing you to move forward with your purchase without any lingering concerns.

3. How to Perform a Title Search

Verifying the legal status of a property before buying it is an essential step. Here’s how you can perform a title search in Singapore:

Step 1: Visit the INLIS Website

The Integrated Land Information Service (INLIS) is where you can access official land records. To begin, visit their website at https://app.sla.gov.sg/inlis/.

Step 2: Choose Your Search Type

Based on your needs, select the relevant option under the Property Information section. You can search for ownership details, property title information, land records, caveat index, and more.

Step 3: Use the Address or Lot Number

You can search by either the property’s address or the Lot Number and Survey District Number. However, note that property addresses in the system are for reference purposes only, as they may not be fully maintained by the Registry. Ensure the address and Lot Number match before proceeding. If they don’t, try searching using a nearby address to identify the correct Lot and Survey District.

Step 4: Conduct a Manual Search (if needed)

While most records are digitised, some properties may not appear online. If this happens, visit the customer service centre at 55 Newton Road, Revenue House, Singapore, to conduct a manual search.

Step 5: Search for Unregistered Land (if applicable)

For land without titles (unregistered land), you’ll need to start with a “Lot Particulars” search. This will provide references to land books and caveat books, and you can then request a printout of the relevant documents.

Step 6: Fees and Payment

Each search request comes with a charge, though no subscription fee is required. Payments can be made via GIRO or credit/debit card.

By conducting a title search through INLIS, you’ll receive essential details about ownership, encumbrances, and legal claims on the property, ensuring that your transaction goes smoothly and securely.

Understanding the Importance of Legal Caveat Checks When Buying Landed Property

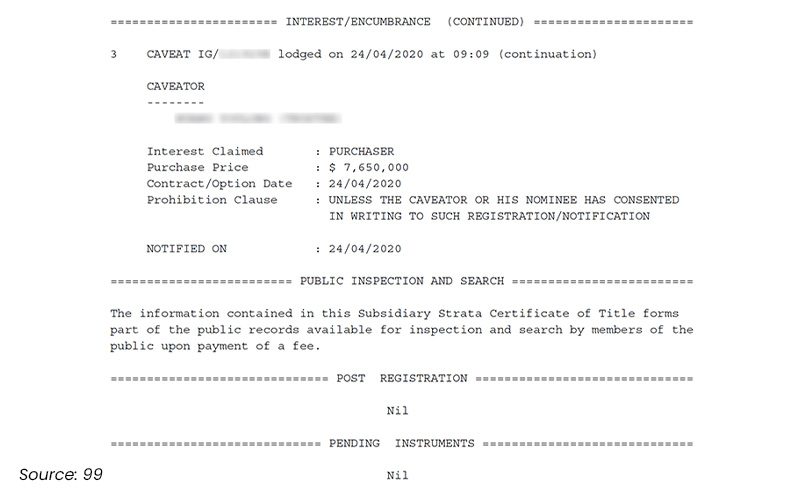

1. What is a Caveat?

A caveat is a legal notice filed with the Singapore Land Authority (SLA) that signals a buyer’s interest in a property. It’s a way for the buyer to stake a claim on the property, preventing others from making a competing offer.

Filing a caveat also helps the buyer identify any existing claims on the property, giving them a clearer picture of its legal standing. This can save time and avoid pursuing a purchase that might not go through due to conflicting interests.

Additionally, a URA caveat search can reveal useful details like recent transaction prices, property-specific information, and market trends. This insight empowers buyers to make more informed decisions and present competitive offers when buying landed property in Singapore.

2. When to Lodge a Caveat

You should lodge a caveat after you’ve exercised the Option to Purchase (OTP) or signed the Sale & Purchase Agreement. This step is typically managed by your conveyancing lawyer, who ensures that your interest in the property is legally protected as you move forward with the purchase process.

3. Process of Lodging a Caveat

Lodging a caveat is done electronically through the Singapore Titles Automated Registration System (STARS). However, only a licensed conveyancing lawyer has access to the necessary account to lodge it on your behalf. Once the caveat is lodged, it takes effect immediately, and the details become publicly accessible.

4. How to Check for Existing Caveats

Before buying landed property in Singapore, it’s critical to check for existing caveats. You can do this through the Singapore Land Authority’s INLIS portal. For a small fee, you can search whether a caveat has been filed against the property. If a caveat is in place, it means the current buyer holds priority, potentially blocking your ability to purchase the property.

5. Who Should Lodge a Caveat?

- Buyers: Always check for existing caveats before proceeding with a purchase. Your lawyer can assist in ensuring that no caveats stand in the way of your transaction.

- Sellers: A buyer’s caveat can demonstrate their commitment to the deal, potentially speeding up the process by establishing trust between both parties.

Performing a caveat check early on helps you avoid complications down the line and ensures a smoother, hassle-free purchasing experience.

Essential Plans and Considerations for Successful Landed Property Projects

When buying landed property in Singapore or embarking on a home build, having the right plans is crucial for regulatory compliance and long-term success. These plans are more than just formalities. They ensure your property meets safety standards and legal requirements while preventing potential setbacks during construction or ownership. From understanding building regulations to planning for utilities, here’s a closer look at the key plans you’ll need.

A. Key Regulatory and Safety Plans

When developing or purchasing a landed property, several key plans help ensure the property meets infrastructure, safety, and environmental regulations:

- Sewerage Interpretation Plan (SIP): This plan details the sewerage systems in place for the property, ensuring waste is managed correctly and complies with national environmental standards. The SIP is essential for maintaining proper sanitation and avoiding legal complications, whether connected to public sewerage or requiring unique waste management systems.

- Drainage Interpretation Plan (DIP): The DIP addresses water drainage and stormwater management, helping to control water flow around the property. This plan prevents flooding and waterlogging by ensuring drainage systems comply with zoning and environmental guidelines, safeguarding the property and surrounding areas.

- Road Line Plan (RLP): The RLP identifies road boundaries and any potential encroachment issues on the property. It ensures that construction or renovation doesn’t interfere with public roads or transport networks, preventing future logistical or legal challenges.

These plans are fundamental for meeting infrastructure needs and maintaining compliance with Singapore’s zoning and environmental regulations. They are also an integral part of A&A works (Additions and Alterations) that ensure the property’s structural integrity and alignment with local regulations, making the development process smoother and more secure.

B. Property and Safety Compliance

When a property is located near sensitive infrastructure like railways or urban developments, additional plans become necessary to safeguard both the structure and its occupants:

- Rail Protection Plan (RPP): For properties close to railways or major transport networks, the RPP is vital in ensuring the construction is equipped with the proper safety measures. This plan protects the property from potential disruptions or accidents caused by nearby transportation systems, providing both security and peace of mind for residents.

- BCA As-Built Architectural and Structural Plans: These plans confirm that the final construction mirrors the approved designs, ensuring full compliance with building codes and safety standards. Typically required for properties undergoing significant renovations or development, these plans are key to meeting the Building and Construction Authority (BCA) guidelines, offering an extra layer of reassurance that the property is in good structural condition and complies with building regulations.

Working closely with a trusted building construction contractor is essential to ensure that these compliance plans are properly implemented. This collaboration helps prevent potential risks, providing both buyers and developers with peace of mind that the property meets the highest safety and regulatory standards.

Understanding Financing Options for Landed Property in Singapore

Securing financing for buying landed property in Singapore requires careful consideration of the available options. Many buyers rely on a combination of CPF savings and bank loans, each offering distinct advantages and conditions. Here’s a closer look at how you can effectively use both CPF and bank loans to finance your property purchase and make the process smoother:

A. Using CPF for Purchase

For Singapore citizens and Permanent Residents (PRs), the Central Provident Fund (CPF) offers a practical way to finance a landed property purchase. Here’s how you can make the most of your CPF savings:

- Down Payment and Monthly Mortgage: Your CPF Ordinary Account (OA) savings can be used to cover the down payment, monthly mortgage payments, and associated fees. This can ease the financial strain, reducing the upfront costs and helping manage payments throughout the loan term.

- Repayment Conditions: Keep in mind that any CPF funds used for the property must be refunded when the property is sold or when the loan is fully repaid. The refund amount includes the funds withdrawn along with accrued interest.

- Limitations: While CPF is an excellent option for financing, its use is capped by the balance in your CPF OA. If your savings are insufficient, this may limit how much you can borrow through CPF.

B. Bank Loan

For many buyers, a bank loan is a common way to finance buying landed property in Singapore. Available to Singapore citizens, PRs, and foreigners, it offers flexibility but comes with specific conditions:

- Loan-to-Value (LTV) Limit: Typically, the Loan-to-Value ratio for residential properties is capped at 75%. This means you can borrow up to 75% of the property’s value, while the remaining 25% must be covered by your own funds, which may include CPF savings or cash. Keep in mind that the LTV ratio could vary depending on the type of property and your buyer profile.

- Interest Rates and Loan Types: Bank loans come with either fixed or floating interest rates. Fixed rates offer predictable payments over a set period, while floating rates change in response to market conditions, potentially offering savings or higher payments. The interest rate will depend on your financial standing and the prevailing market trends.

- Non-Residents: For foreigners, securing a bank loan may be slightly more challenging. They may face lower LTV ratios, requiring a larger down payment and higher interest rates. Additional documentation is often required to demonstrate financial stability and repayment ability.

How to Choose Between CPF and Bank Loans

When buying landed property in Singapore, deciding whether to use your CPF savings or secure a bank loan often comes down to your financial situation and long-term plans. Here’s a breakdown to help guide your choice:

CPF:

- Pros: CPF offers a lower interest rate of 2.5% per annum for CPF OA funds, making it a more cost-effective option in the long run. There’s also flexibility in the repayment structure, and no strict credit checks are required for eligibility. If you have enough CPF savings, it’s a great way to reduce the loan amount you need to borrow.

- Cons: Your CPF savings are limited by your Ordinary Account balance, so you may not be able to fully cover the property’s price. Additionally, any CPF funds used must be returned, along with accrued interest, when you sell the property or repay the loan.

- Pros: CPF offers a lower interest rate of 2.5% per annum for CPF OA funds, making it a more cost-effective option in the long run. There’s also flexibility in the repayment structure, and no strict credit checks are required for eligibility. If you have enough CPF savings, it’s a great way to reduce the loan amount you need to borrow.

Bank Loans:

- Pros: Bank loans typically offer higher loan limits and more flexibility in repayment terms. If your CPF savings don’t cover the full cost of the property, a bank loan can help you bridge the gap. Foreign buyers can also access bank loans, though they face stricter conditions.

- Cons: Bank loans come with higher interest rates compared to CPF, meaning the total cost of the loan will likely be higher. The repayment terms are more rigid, and securing a bank loan may involve additional paperwork and documentation.

- Pros: Bank loans typically offer higher loan limits and more flexibility in repayment terms. If your CPF savings don’t cover the full cost of the property, a bank loan can help you bridge the gap. Foreign buyers can also access bank loans, though they face stricter conditions.

For many buyers, a combination of CPF savings and a bank loan is an ideal solution. You can use your CPF savings for part of the down payment and take a bank loan for the remaining amount. This way, you will benefit from both financing options.

Key Financial Considerations When Buying Landed Property

Buying landed property in Singapore involves careful financial planning to ensure the property is within your budget and aligns with regulatory requirements. Beyond securing financing, it’s essential to evaluate your long-term financial health and make well-informed decisions. Here’s a closer look at the key financial factors to consider:

1. Down Payment

The down payment is a crucial step in the property buying process and typically amounts to at least 25% of the property’s value. It’s the initial investment that secures your claim on the property. Here’s a breakdown of what it entails when buying landed property in Singapore:

- Portion in Cash: At least 5% of the down payment must be paid in cash, ensuring you have the liquidity to cover the immediate costs. This upfront cash payment helps demonstrate your financial readiness.

- Remaining Payment Options: The remaining 20% can be covered using your CPF Ordinary Account (OA) savings or your own funds, depending on your financial situation. Opting for CPF can reduce the strain on your finances, but remember, any CPF funds used must be refunded when the property is sold or the loan is fully repaid.

- Additional Costs: Beyond the down payment, other upfront costs, such as stamp duty, legal fees, and valuation fees, should also be factored into your budget. While often overlooked, these expenses are part of the total financial picture.

2. Mortgage Loan

For most property buyers, a mortgage loan is the primary way to finance the bulk of the property price. Typically, the loan amount is capped at 75% of the property’s value, and the loan terms will determine how much you pay each month. Here’s a deeper dive into mortgage loans when buying landed property in Singapore:

- Loan-to-Value (LTV) Ratio: As mentioned earlier, the LTV ratio for a residential property is typically 75%, meaning you’ll need to fund the remaining 25% through your down payment (either in cash or CPF). This ratio can shift depending on your financial profile and whether you’re purchasing a new or resale property.

- Repayment Terms: Your monthly mortgage repayment depends on the loan amount, interest rate, and loan tenure, which usually spans 20 to 30 years. Opting for a shorter tenure will result in higher monthly repayments but less interest paid overall. On the other hand, a longer tenure lowers monthly payments but increases the total interest paid over time.

- Interest Rates: The interest rate plays a significant role in shaping your monthly repayment. Banks typically offer either fixed or floating rates. Fixed rates provide stability over a set period, while floating rates adjust with the market, offering potential savings or risk depending on economic conditions and your financial profile.

3. Income Requirements and Total Debt Servicing Ratio (TDSR)

The Total Debt Servicing Ratio (TDSR) is a crucial factor that banks use to evaluate your ability to repay a mortgage loan. It’s a regulatory measure designed to ensure that borrowers don’t take on too much debt in relation to their income. Here’s how the TDSR works when buying landed property in Singapore:

- TDSR Limit: The TDSR limits your total monthly debt commitments (including your mortgage, credit card bills, car loans, and other debts) to 55% of your monthly income. For example, if you earn $10,000 a month, your total debt obligations cannot exceed $5,500.

- Income and Loan Affordability: The higher the property value you’re eyeing, the more income you’ll need to qualify for a mortgage. If you have existing debts, such as car loans or credit card balances, they’ll eat into the portion of your income available for the property loan, making it harder to qualify for a larger loan amount.

- Impact of TDSR on Loan Eligibility: The TDSR plays a pivotal role in determining your eligibility for a mortgage. Suppose your debt obligations surpass 55% of your income. In that case, you may not qualify for a loan or be only eligible for a smaller loan amount, limiting your options when buying landed property in Singapore.

Understanding the financial landscape, including TDSR, down payment requirements, and mortgage loan structures, will help you assess your ability to comfortably manage your property purchase. Be sure to account for both initial and ongoing costs to ensure your investment remains financially viable in the long term.

Learn more: Buying a landed house in Singapore

Questions You Might Have

Purchasing landed property in Singapore involves a lot of moving parts, and it’s natural to have questions along the way. To help clarify some common concerns, here are a few questions that potential buyers often have during the process of buying landed property in Singapore:

1. Can I Rent Out My Landed Property?

Yes, renting out your landed property is possible, but there are some key things to consider. First, check your area’s zoning regulations. Some neighbourhoods, especially conservation zones or tightly regulated areas, may have restrictions on rentals. If your property is leasehold, the lease terms may also impact your ability to rent it out, particularly if the lease has a short remaining duration. Additionally, renting requires compliance with local rental laws, which include registering your tenant with the authorities and ensuring transparent and fair lease terms. To stay on the safe side, it’s wise to consult a legal professional to guide you through the necessary steps.

2. How Long Does the Buying Process Take?

The time it takes to purchase a landed property can vary, but on average, it typically spans 8 to 12 weeks, from making an offer to finalising ownership. Once you’ve agreed on the price, the seller will issue you an Option to Purchase (OTP), usually with a 1% option fee. You’ll have up to 14 days to decide whether to move forward by exercising the OTP, which involves paying the remaining 4% deposit.

After that, you’ll conduct due diligence, such as title searches, and secure financing if necessary. The final stages involve signing the Sale and Purchase Agreement (S&P) and making the full payment upon completion. Keep in mind that the process may take longer for Permanent Residents (PRs) or foreigners, as additional government approvals may be required. Unexpected issues can also arise, so it’s a good idea to allow some flexibility in your timeline when buying landed property in Singapore.

3. What Are the Risks of Buying Landed Property?

As with any investment, buying landed property in Singapore carries certain risks. One of the biggest is the fluctuation of property values. Economic shifts, changes in demand, and other factors can affect property prices. For instance, a slowdown in the economy or an increase in interest rates may lead to a decline in property values, potentially impacting your long-term investment.

Another factor to consider is the maintenance costs. Larger properties, like bungalows or Good Class Bungalows (GCBs), can be expensive to maintain, especially if they feature extensive gardens or require frequent upkeep. Lastly, the resale potential of the property is vital to think about. Some properties in less desirable locations might not sell as easily or quickly, so it’s essential to carefully research the area, property condition, and market trends before committing to the purchase.

4. Can PRs and Foreigners Buy Landed Property in Singapore?

Yes, but with certain conditions:

- Singapore Citizens have no restrictions and can freely purchase any type of landed property, with the option to use CPF for financing.

- Permanent Residents (PRs) must obtain the Singapore Land Authority (SLA)’s approval to buy landed homes. While they can generally purchase terrace houses, semi-detached homes, and bungalows, specific conditions apply.

- Foreigners face the strictest restrictions. They can only buy landed property in Sentosa Cove (with SLA approval), or certain strata landed homes in approved condominium developments. For other types of landed property, they must apply for special approval, which is not always granted.

Conclusion

Buying landed property in Singapore is an exciting and rewarding investment, but it requires careful planning and expert guidance. From securing financing to navigating legal requirements and managing construction projects, every step is essential to ensuring a successful investment.

Armed with the right knowledge and support, you’ll be able to make decisions that positively impact your future. Whether you’re improving your property or designing your dream home, partnering with a trusted house design contractor can help bring your vision to life and make the process smoother.

If you’re ready to bring your vision to life or need professional assistance with property additions or alterations, Sim The Builder is here to help. With our expert design & build services and commitment to quality craftsmanship, we can transform your property to suit your unique needs.

Contact us today to discuss how we can make your dream home a reality. Our team is here to assist you at every stage of the process.